pedoman main judi poker yg komplit & aman utk pemula-Di internet telah tidak sedikit dijelaskan seperti apa trick main judi poker online komplit dgn petunjuk utk meraih kemenangan, memang lah benar permainan judi poker sedikit susah utk di pahami & dikuasai oleh para penjudi pemula dgn argumen tak tahu kombinasi paling besar & seperti apa trik bermainnya. Nah kepada peluang yg indah ini kami bakal sedikit share berita terkait bersama beberapa elemen yg berhubungan bersama permainan judi poker supaya kamu memang sanggup mendalami gimana trick jalannya permainan dalam judi poker online di internet, sebelum kita masuk ke trik main-main judi poker online di internet, lebih baik kita simak apalagi dulu beberapa aspek yg butuh kamu pahami dgn benar.

mula-mula ialah istilah dalam permainajn judi poker. Ada beberapa istilah yg butuh kamu pahami, perdana yakni blind – Blind sendiri adalah nilai besar nya ante tiap-tiap meja poker, yg mana ada blind mungil & blind agung. Blind mungil yaitu setengah dari blind agung. contohnya saja buat meja bersama blind akbar 5000 maka blind kecilnya yakni 2500. Ini menandakan bahwa ante perdana yg mesti & wajib dibayarkan ialah 2500 – 5000. seterusnya istilah lain dalam permainan judi poker ialah simbol dealer, ini menandakan bahwa player memiliki peluang jadi seseorang dealer, utk player yg mempunyai simbol dealer, mereka tak diharuskan utk mengikuti permainan bersama membayar ante. setelah itu istilah lain dalam permainan judi poker sendiri merupakan kombinasi card. Kombinasi card ini pass tentukan kemenangan dari tiap-tiap pemain yg main judi poker online di internet. Berikut ialah beberapa kombinasi card poker online yg tetap dimanfaatkan hingga ketika ini. perdana ialah kombinasi card royal flush yg ialah kombinasi card bersama bunga yg sama bersama urutan angka penting yg sama contohnya ( AKQJ10 + Bunga sama ) seterusnya kombinasi card terendah dalam permainan judi poker online sendiri merupakan high kartu.

Nah dari situ kamu pastinya telah paham sebelum masuk ke trik main-main judi poker online di internet, berikut yakni tahapan kalau kamu mau tahu seperti apa trik main judi poker online di internet. perdana yg mesti kamu laksanakan merupakan dgn mendaftarkan lebih-lebih dulu ke web agen judi poker online terpercaya yg ada di Indonesia, sesudah itu mari melaksanakan deposit bersama akbar minimal & maksimal dari website yg kamu ikuti, sesudah proses deposit & konfirmasi selesai. kamu baru dapat memainkan permainan judi poker di internet. memilih type meja yg mempunyai jumlah taruhan jauh lebih mungil dari jumlah dana yg kamu punyai, ini bermanfaat buat menekan kekalahan yg dapat berjalan, duduk terhadap kursi yg kamu yakini sanggup memberikan kemenangan. Dari sini kamu mampu mulai sejak main-main bersama player lain, usahakan buat main-main di meja dgn jumlah player 8 orang, tujuannya biar kemenangan yg didapatkan serta lumayan agung. jangan sampai lupa buat membeli jackpot yg ada dibagian bawah permainan, mutlak buat pembelian jakcpot ini apabila sewaktu-waktu kamu mendapati kombinasi card keren maka tak bakal sia-sia.

Nah itulah kiat komplit & sederhana utk main judi poker online di internet yg gampang utk kita pahami, mudah-mudahan bersama kiat ini kamu dapat memperoleh kemenangan dari main-main judi poker online di internet. Ok hingga disini lalu kabar ini mudah-mudahan lumayan memberikan pembelajaran terkait bersama judi poker online di internet.

2017 SVCIP Forum - Public Policy Proceedings

Background

This blog entry summarizes key themes and discussion points shared during the Silicon Valley Competitiveness and Innovation Project 2017 Public Policy Forum, held at Microsoft’s Silicon Valley campus in Mountain View, California on March 3, 2017. More than 190 participants attended the forum, including C-level executives, elected officials, education leaders and other community members.

Overview Of Silicon Valley Competitiveness and Innovation Project

Now in its third year, the Silicon Valley Competitiveness and Innovation Project (SVCIP) is a research initiative co-managed by the Silicon Valley Leadership Group and Silicon Valley Community Foundation. SVCIP tracks multiple economic and quality of life indicators to assess and evaluate Silicon Valley’s business and innovation competitiveness against other national and international “innovation regions.” Designed to coincide with the beginning of California’s two-year legislative cycle, the 2017 public policy forum is convened to engage community leaders and obtain feedback on best strategies for SVCIP advocacy.

Forum Structure

Leadership Group CEO Carl Guardino and SVCF Board Chair Samuel Johnson, Jr. opened the forum with a welcome and provided an overview of the event. SVCF’s Chief Community Impact Officer Erica Wood and Leadership Group Senior Vice President Dr. Brian Brennan then presented a data-based update on report indicators. California Lieutenant Governor Gavin Newsom provided a keynote discussion on public policy opportunities. The Lieutenant Governor then joined a panel moderated by Carl Guardino to discuss the region’s innovation and competitiveness with Silicon Valley Bank CEO and Leadership Group Board Chair Greg Becker, Genentech Vice President Carla Boragno, Microsoft Corporate Vice President and SVCF Board Member Dan’l Lewin, and Education Trust-West Executive Director Ryan J. Smith.

Participants then engaged in breakout conversations to address one of seven policy areas in which they had indicated interest during their registration. Participants were specifically asked to identify two to three attainable and realistic policy approaches that could be accomplished within the next 18 months. The event ended with a brief report out from each conversation and organizers’ commitment to capture and disseminate discussion content. The following section summarizes the approaches identified within each discussion group, and do not necessarily reflect the policies or priorities of SVCF or the Leadership Group.

Breakout Session Proceedings

- Housing

- Sacramento needs to implement an incentivize affordable and accessible housing. (AB 71, SB2)

- Pass legislation to secure $ for affordable housing (AB 71(Chiu) and SB 2 (Atkins)

- Find way to revenue share property taxes

- State needs to pass local accountability measures – by-right and requiring building planned for in housing elements and RHNA.

- Education

- Teacher shortage:

- Create streamlined pathways into the profession for new teachers and mid-career

- Use tech to facilitate teaching and delivery

- Differential pay to incentivize

- Improve the narrative around teaching

- Early childhood development

- High quality early childhood education for all

- Align to k-12 system

- Funding

- R&D funds for local education innovation

- Restructure tax (Prop 13) and funding distribution

- Pension reform

- Clearinghouse for public-private partnerships

- Teacher shortage:

- Transportation

- Electrify Caltrain

- Transit Agency Coordination

- 9-County Transportation Measure

- Workforce/Higher Education

- Summer program that brings together a task force to solve issues of affordability, access, and curriculum alignment with industry needs – with members from industry, community colleges, 4-year institutions, and K-12 entities.

- Summer program – Professional development that links professionals in industry with educators, makes it easier for talented industry folks to teach, and provides opportunities for teachers to work in industry temporarily (like Ignited).

- Make sure that the first two initiatives are industry-led, so that it can define the skills needed, and inform and fund the process.

- R&D/Innovation

- R&D: increase funding, focus on supply chain

- STEM initiatives

- Replicate Genentech models of hands-on learning

- Focus on addressing the skills gap in the high tech manufacturing workforce

- Entrepreneurship

- 6 entrepreneurship challenge events, outreach with/to local community colleges, innovation challenges, friendly competition and create inclusive tech ecosystem

- Workforce development and training for emerging leaders (students)

- Policy-specific: housing, immigration

- Tax/Regulation

- Prop 13 reform (how property is valuated)

- Debt forgiveness for teachers in STEM

- Incentives for students to have access to STEM and the treatment of computer science as math.

Poverty, Wealth and California’s Migration Flows

By Brian Brennan

The primary takeaway from the immigration data in the 2017 Silicon Valley Competitiveness & Innovation Report – released last week at Microsoft in Mountain View – is that people keep coming to the Valley. Despite demoralizing commutes and onerous housing prices, there is a steady stream of newcomers from abroad – nearly 2,800 a month in 2015.

The domestic migration dynamics between Silicon Valley and the rest of the United States are more complicated. Net domestic migration to the Valley is negative (-832 in 2015), but that number itself masks a larger narrative that is revealed in a report earlier this week from the Sacramento Bee about California’s migration patterns – two narratives, in fact.

The first is about geography: Domestic migration to California between 2000 and 2015 was driven by movement from states east of the Mississippi – primarily the Mid-Atlantic states and New England, as well as Michigan, Florida, Illinois and Alabama. Those moving away from California over that same period tended to stay in the west, heading in largest numbers to Texas (155,343), with Oregon, Nevada and Arizona not far behind.

The second narrative involves income. The Bee’s data reveal that the poor are leaving California while those with means are drawn to the state:

All told, California lost about 260,000 economically disadvantaged residents to the 10 states with the lowest cost of living (from 2000 to 2015), compared to a net gain of about 40,000 from the 10 states (other than California) with the highest cost of living.

These dynamics have consequences. They mean a more socioeconomically segregated region. They mean a hollowing-out of a middle and working classes that are essential to any community. And they mean additional pressure on even successful companies to consider growing outside of California.

They are also not inevitable. They are driven by many things, not least policy constraints on housing supply. Our policymakers are facing many pressing challenges, but when Silicon Valley’s employment rises nearly 25% and population rises 6.4%, as it did between 2010 and 2015, while housing stock increases by only 2.6%, the outcomes are predictable: an elite, segregated region with an unbalanced economy that drives too many away.

Dr. Brian Brennan is Senior Vice President at the Silicon Valley Leadership Group.

How Does Silicon Valley Compare With Other Global City-Regions?

By John Melville

Most would agree that Silicon Valley is one of the world’s leading innovation regions. But what do the numbers say? Unfortunately, comparable international measures are still not available in many issue areas covered by SVCIP. That is why we have been able to develop comprehensive comparisons only across selected Innovation Regions in the United States. However, we do recognize Silicon Valley competes in a global innovation economy, and should be measured against global regions whenever possible.

Here is what we do know: As we reported in the 2016 SVCIP Update, the Compass’ Global Startup Ecosystem Ranking of 2015 placed the region first based on a composite measure incorporating venture capital investment, start-up company exit valuations, talent pool, and entrepreneurial supports and networks. At the same time, other regions like Berlin, London, Tel Aviv, Chicago, and Boston scored higher on the Growth Index, meaning they are making up ground on Silicon Valley in these areas.

The Brookings Institution has just released a comprehensive analysis of the 123 largest metropolitan areas in the world (see Redefining Global Regions, 2016). On a variety of indicators, the San Jose and San Francisco metropolitan areas rank among the top regions in the world. In short: Silicon Valley has the largest share of publications in the top 10% of cited papers (2010-2013), and generates the most patents per capita. It is the most productive region, and attracts the largest venture capital investment per capita of any metropolitan area in the world. It has among the highest percentage of people with bachelors’ or higher degrees, only exceeded by Singapore, London, and Washington D.C.

Despite being the birthplace of many founding internet technologies, one of the measures on which the region performs poorly is average internet download speed. Silicon Valley is actually well behind several regions across Asia (e.g., Singapore, Tokyo, Osaka, Nagoya, Seoul, Hong Kong), Europe (e.g., Paris, Stockholm, Amsterdam, Barcelona, Copenhagen, Zurich), and the United States (e.g., Austin, Seattle, Boston, New York City, and Los Angeles, as well as Baltimore, Philadelphia, Kansas City, St. Louis, and Riverside).

Stay tuned for the 2017 SVCIP Update which will be released in February.

John Melville is Co-CEO of Collaborative Economics.

Pathways to Continued Prosperity – Expand the STEM Pipeline

By PK Agarwal

The 2016 Silicon Valley Competitiveness and Innovation Project reports that the Silicon Valley Region’s foundations of prosperity are showing some signs of stress. The report compares key data for innovation regions in the U.S. including the New York City metro area, Boston, Southern California, Seattle and Austin, as well as a select number of global areas.

The troubling indicators cited for Silicon Valley were an outflow of talent to other parts of the U.S., increased labor costs and slower growth in STEM degrees. The success of our Region is understandably tied to the availability of high quality STEM talent. The slowdown of growth in STEM degrees is a particularly alarming indicator, as this is a harbinger of the increasing talent gap. During the 2013-2014 period, growth in STEM degrees was the lowest in Silicon Valley, 4.8% compared to 11.4% in Seattle, 11.2% in New York and 9.6% in Boston. At the same time, our share of foreign born workers was the highest of any of the report’s identified innovation regions. This appears to indicate that we are starting to fall behind in the race for the STEM talent. This indicator is all the more troubling considering that a Whitehouse report points out that the IT demand-supply gap is expected to continue to grow at least through 2020.

The STEM pipeline issues go a lot deeper than at the college level. Take a look at the eighth grade math proficiency. In 2014, slightly less than half (49%) of students met or exceeded the state standards for math, based on the Common Core education standards. The “diversity challenge” in the STEM pipeline is illustrated by the fact only 20% of African American students and 21% of Latino students met these standards. Eighth grade math proficiency is a crucial indicator of college preparedness and subsequent professional STEM pipeline.

One of the innovative answers to the region’s STEM shortage and diversity challenge is to re-skill non-STEM professionals into STEM fields. A number of educational institutions are coming up with programs to open the STEM pipeline to people who have already obtained non-STEM college education. We, at Northeastern University- Silicon Valley, are one of those innovators. Our ALIGN program addresses the talent issue by providing non-STEM undergrad degree holders a pathway to a Master’s degree in Computer Science or Cybersecurity. It is well understood that people with a variety of multi-disciplinary skills bring a unique perspective to the workplace. Accordingly these ALIGN students, with a wide range of academic and cultural backgrounds, bring new vistas to the STEM disciplines. Plus, they tend to excel in soft skills, which differentiates them in the workplace. Finally, programs such as ALIGN provide a tool to deal with the diversity issue in Silicon Valley.

The availability of skilled workforce is the critical asset that will keep Silicon Valley growing and thriving. Industry and academia need to partner and innovate to solve the pipeline issue in the short-term as well as long-term.

P.K. Agarwal is Regional Dean and CEO of Northeastern University-Silicon Valley and former CTO for California under Governor Schwarzenegger.

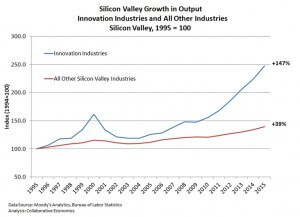

Innovation Industries Drive Silicon Valley’s Economy

By John Melville

The Silicon Valley Competitiveness and Innovation Project (SVCIP) focuses on a subset of industries in the regional economy that are important export-oriented sectors with positive ripple effects on other parts of the economy. We call them “innovation industries” because innovation is their shared core business. While their products and services vary widely—from software to hardware, internet-based services to biotechnology, and many more—what they also share is a core need to operate in a supportive community environment, including talent, financing, and other resources. Thus, their success is an important measure of how well Silicon Valley and other regions are providing an effective “innovation ecosystem.”

The Silicon Valley Competitiveness and Innovation Project (SVCIP) focuses on a subset of industries in the regional economy that are important export-oriented sectors with positive ripple effects on other parts of the economy. We call them “innovation industries” because innovation is their shared core business. While their products and services vary widely—from software to hardware, internet-based services to biotechnology, and many more—what they also share is a core need to operate in a supportive community environment, including talent, financing, and other resources. Thus, their success is an important measure of how well Silicon Valley and other regions are providing an effective “innovation ecosystem.”

So how are we doing? Between 1995 and 2015, output in Innovation Industries rose by almost 150%, while that of the rest of the economy increased by less than 40%. A decade ago output for the both sets of industries were actually rising at a comparable rate. This situation changed significantly when Innovation Industry output accelerated rapidly beginning in 2010, a trend that has continued through at least 2015.

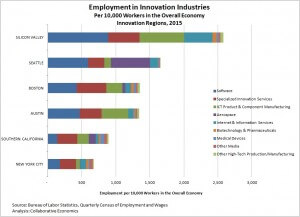

What about jobs? Silicon Valley has the highest proportion of Innovation Industry jobs per capita compared to other Innovation Regions. Be sure to stay tuned for the release of the SVCIP 2017 Update report to be released early next year to learn more about how jobs in Silicon Valley Innovation Industries are also growing faster than those in other Innovation Regions.

What about jobs? Silicon Valley has the highest proportion of Innovation Industry jobs per capita compared to other Innovation Regions. Be sure to stay tuned for the release of the SVCIP 2017 Update report to be released early next year to learn more about how jobs in Silicon Valley Innovation Industries are also growing faster than those in other Innovation Regions.

John Melville is Co-CEO of Collaborative Economics.

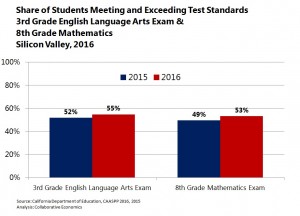

More Students Meeting Math and Language Arts Standards, But Many Fall Short

By John Melville

In 2016, 1,140 more Silicon Valley 8th graders met or exceeded state standards in mathematics. That meant 53% of all local 8th graders now meet the Smarter Balanced math standards (see below), up from 49% in 2015. On this measure, Silicon Valley outpaces California by a wide margin. In 2016, just 36% of California 8th graders met the math standard compared to 53% of Silicon Valley 8th graders. And, the gap is widening: California’s percentage of students meeting or exceeding the state standard rose from 33% in 2015 to 36% in 2016 while the Valley’s increased from 49% to 53%, respectively.

This is good news to a point. Certainly, more local 8th graders increased their chances of becoming part of the Valley’s STEM workforce. However, in 2016 the achievement gap in mathematics by ethnicity in Silicon Valley remained striking: only 24 percent of African American and 25 percent of Hispanic or Latino 8th graders met or exceeded the state standards on the Smarter Balanced mathematics exam. At the same time, 82 percent of Asian students and 68 percent of Caucasian students met or exceeded the standard.

The 8th grade math achievement gap didn’t change much between 2015 and 2016. In 2015, 20% of African American and 21% of Hispanic or Latino students met or exceeded the state standard, while 79% of Asian and 66% of Caucasian students met or exceeded the standard. This means the largest gap was 59% in 2015 compared to 58% in 2016.

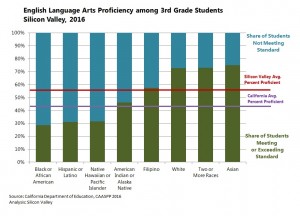

It’s a similar story when it comes to the performance on Silicon Valley 3rd graders in language arts. The overall percentage of local 3rd graders meeting or exceeding the Smarter Balanced standard rose from 52% in 2015 to 55% in 2016. While California’s rate rose too, the gap between Silicon Valley (55% in 2016, up 3% from 2015) and the State (42%, up 4% from 2015) remains large.

In 2016, higher proportions of Silicon Valley 3rd grade students across all ethnicities met or exceeded the state Smarter Balanced standard for English Language Arts compared to the previous year. Notably, the proportion of Hispanic and Latino students (accounting for 38 percent of 3rd grade test takers) that met or exceeded the state standard rose by 4.6 percent in 2016. The achievement gap by ethnicity was slightly less pronounced in Silicon Valley in 2016 than 2015, though remained large (46 percentage points) between Asian students (which as a group had the highest proportion of students meeting and exceeding the standard) and African American students (which as a group had the lowest proportion).

Bottom line? There has been a lot of attention on math and reading in the early grades—and there appears to be progress overall. Smarter Balanced is aligned to the Common Core state standards, and educators have had time to adapt and students have had 3 years of instruction based on those standards. But, large numbers of local students are still falling short of statewide standards, and are not on a path to participate in high-skill jobs created by Silicon Valley’s innovation economy. What more can we do to close these achievement gaps? Share your experience about what works and what you think needs to be done.

Smarter Balanced is an assessment system developed to align with the Common Core standards, which are “challenging students to understand subject matter more deeply, think more critically, and apply their learning to the real world. To measure these new state standards, educators from Smarter Balanced states worked together to develop new, high-quality assessments in English and math for grades 3–8 and high school. These Smarter Balanced assessments provide more accurate and meaningful information about what students are learning by adapting to each student’s ability, giving teachers and parents better information to help students succeed in school and after.” (see www.smarterbalanced.org).

John Melville is Co-CEO of Collaborative Economics.

The STEM Core: Moving Silicon Valley’s Existing Students onto Engineering and Computer Science Degree Pathways

By Dave Gruber, Gabe Hanzel-Sello and Caz Pereira

In his October 3rd blog post, John Melville of Collaborative Economics makes the point that Silicon Valley is not producing enough STEM Degree candidates.

One of the great sources for the next generation’s STEM Workforce are our regional community colleges. The Bay Area has 23 community colleges, 11 in Silicon Valley alone. State data suggests that 80% of students entering these colleges begin with remedial math and English courses. Statewide experience suggests few of these students will pursue pathways needed to qualify for the kinds of jobs in engineering and computer science that are available now and in the near-future. In fact, statewide data shows that of students entering community college at remedial levels, only 1% ever reach calculus proficiency- a foundation prerequisite for engineering and computer science degrees. In addition to breaking through the calculus barrier, these students are faced with the same challenges of too many Silicon Valley residents; lack of STEM professional role models, lack of knowledge of STEM career and educational opportunities, and lack of the social, financial and academic support needed to complete a rigorous STEM education pathway. This pool of students, many of them the first in their family to go to college, reflects the diversity of California and, because they’re already living in Silicon Valley, represent an ideal solution to the regional need for a homegrown, diverse workforce. Despite this current opportunity, few current efforts are aimed at encouraging and assisting these specific students to connect with the vast range of STEM job opportunities.

One exciting new initiative to realize the potential of this next generation local STEM workforce is the Silicon Valley Engineering Technology Pathways (SVETP); a $13 million initiative led by San Jose Evergreen Community College District and funded by the State of California Department of Education’s Career Pathways Trust. SVETP supports a new strategy, “The STEM Core”, designed specifically to address the challenges of assisting remedial-level community colleges to pursue B.S. degree pathways in engineering, computer science, and related STEM fields. In place of individual students pursuing remedial coursework, the STEM Core, now being implemented at 9 local community colleges, creates a cohort-based learning community of students with a common goal of achieving calculus readiness, workplace competency, and paid industry internships within one year. The STEM Core model differs from traditional community college education in the following critical ways; 1) Students are placed into a block-scheduled, cohort-based learning community, 2) In place of isolated, remedial math courses, students pursue an accelerated math sequence compressing 3-4 traditional math courses into one year. To engage students, coursework is contextualized to real-world engineering and computer science applications, 3) Students gain access to engineering and computer science classes usually closed to them as well as industry speakers and field trips, 4) Students are assisted by a dedicated Student Support Specialist who helps them in adjusting to the rigors of community college education including development of study skills, career orientation, and dealing with the issues of transportation, family life, and health that so often derail community college students, and 5) In addition to the academic curriculum students have the opportunity for hands-on, paid summer internships at partner employer sites.

In pilot programs conducted at four colleges around California over the last four years, this approach has shown strong early promise in directing students on a STEM pathway. 65% of remedial students entering the program reached Calculus within one year (compared to 4% statewide over three years). In addition, students have been successfully placed at over 200 internship opportunities provided by employers such as NASA Ames, Lawrence Livermore National Lab, NASA Jet Propulsion Laboratory, and Type A Machines. A surprising number of students were able to convert their initial grant-funded internship into a company-sponsored part time job. Most importantly, the STEM Core experience is leading a new pool of students to pursue the STEM degrees that are vital to their future and that of the larger Silicon Valley economy.

Dave Gruber, Gabe Hanzel-Sell and Caz Pereira are with Growth Sector.

Filling Our Talent Pool: Strong Record, But Missed Opportunity?

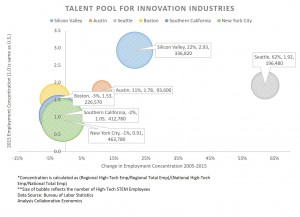

Silicon Valley has an enviable track record of filling (and sometimes refilling) our pool of tech workers year after year. This is important because Science, Technology, Engineering, and Math (STEM) talent is a key competitive asset in innovation regions as STEM skills are critical in researching, developing, improving, and scaling innovative technologies, business and processes. Today, our region has a large absolute number of STEM workers compared to other innovation regions.

Silicon Valley also has a much higher concentration of STEM talent than many other innovation regions—that is, the proportion of STEM workers in the overall workforce relative to the national average. Absolute numbers are important, but high concentration is too—indicating a strong specialization in STEM talent-driven industries in the regional economy. Some regions have large absolute numbers but low concentrations (e.g., Southern California, New York City region), while others have higher concentrations but lower absolute numbers (e.g., Seattle, Boston, Austin). Silicon Valley actually ranks among the highest on both measures.

Not surprisingly, the Valley is almost three times more concentrated in STEM workers than the nation as a whole. But, it is also almost 50% more concentrated than the Boston region, and close to 40% more than Seattle and Austin. While Southern California and the New York City region both have larger absolute numbers of STEM workers, they have a much smaller concentration of such workers given their overall labor forces.

As important, Silicon Valley has grown its STEM advantage over the past decade. Between 2005 and 2015, the region’s concentration of STEM talent grew 22%. Of the comparison regions, only Seattle’s concentration increased at a faster rate. Austin’s pool grew at half the rate of the Valley. And, strikingly, Boston, Southern California, and the New York City region all lost ground, as their concentration of STEM workers actually declined.

As important, Silicon Valley has grown its STEM advantage over the past decade. Between 2005 and 2015, the region’s concentration of STEM talent grew 22%. Of the comparison regions, only Seattle’s concentration increased at a faster rate. Austin’s pool grew at half the rate of the Valley. And, strikingly, Boston, Southern California, and the New York City region all lost ground, as their concentration of STEM workers actually declined.

Overall, a good news story, right? Yes, Silicon Valley has a strong record of expanding its technical talent base. So, what is the missed opportunity?

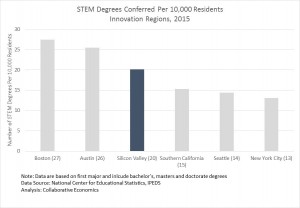

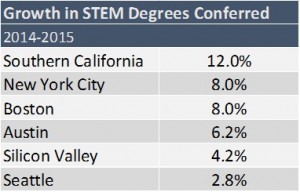

If we look at the local production of STEM degrees—preparing local residents for Silicon Valley STEM jobs—we find a different story. Instead of leading the pack, the region ranks behind Boston and Austin, and just ahead of Southern California, Seattle, and the New York City region in the number of STEM degrees conferred per capita. And, STEM degree production per capita in Southern California and the New York City region grew much faster than that of Silicon Valley between 2014 and 2015. Boston’s STEM degrees conferred per capita also grew twice as fast as our region.

If we look at the local production of STEM degrees—preparing local residents for Silicon Valley STEM jobs—we find a different story. Instead of leading the pack, the region ranks behind Boston and Austin, and just ahead of Southern California, Seattle, and the New York City region in the number of STEM degrees conferred per capita. And, STEM degree production per capita in Southern California and the New York City region grew much faster than that of Silicon Valley between 2014 and 2015. Boston’s STEM degrees conferred per capita also grew twice as fast as our region.

Why is this important? We are clearly able to fill our STEM talent pool better than most. It is important because we have the opportunity to prepare local residents to join our technical talent pool and enjoy the benefits of our regional prosperity. But, the ticket to play is a STEM degree. While STEM degree production in Silicon Valley is growing, it is not growing as fast as many innovation regions. We will need to do better if we are to capitalize on this “local sourcing” opportunity.

Why is this important? We are clearly able to fill our STEM talent pool better than most. It is important because we have the opportunity to prepare local residents to join our technical talent pool and enjoy the benefits of our regional prosperity. But, the ticket to play is a STEM degree. While STEM degree production in Silicon Valley is growing, it is not growing as fast as many innovation regions. We will need to do better if we are to capitalize on this “local sourcing” opportunity.

Let us know what you think—including your suggestions for how our region can help local residents attain STEM degrees and join our technical talent pool.

John Melville is Co-CEO of Collaborative Economics

Funding R&D at Local Universities: What is Our Commitment to the Innovation Pipeline?

Research and development expenditures at local universities is an indicator of our nation’s commitment to seeding the innovation pipeline. New ideas—some with commercial applications—flow forth from U.S. academic centers, particularly in strong innovation regions like Silicon Valley. So, how are we doing? The latest numbers are in. The story is mixed.

The long-term trend nationally has been positive. Over the past decade, between 2005 and 2014 (the latest data available), R&D expenditures at U.S. universities grew an inflation-adjusted 17%. However, between 2013 and 2014, the amount of total R&D funding at U.S. universities actually dropped from $68.1 billion to $67.2 billion.

Some innovation regions have done much better than the nation as a whole over the past decade. New York City metropolitan area substantially outperformed the national average over the past decade, increasing its university-based R&D expenditures by 68% between 2005 and 2014. So too did Boston (+34%) and Seattle (+26%).

Silicon Valley, however, did not kept pace with the national average, increasing its R&D expenditures only 12% during the past decade. Our region did outpace Austin (+10%) and Southern California (+9%).

Was the New York City metro area’s rapid rise really the result of a large percentage gain from a small base? No, the region recorded a total of $3.6 billion in university-based R&D funding in 2014, larger than the totals in Boston and Silicon Valley, and well ahead of those in Seattle and Austin.

Taking a closer look at what happened in 2014, only Silicon Valley and New York City metro universities did better than the nation as a whole. Silicon Valley’s R&D expenditure rose one percent between 2013 and 2014 while the R&D fell one percent across all U.S. institutions. New York City experienced the fastest annual growth in R&D expenditures of the comparison regions (+7%) while levels in Boston, Seattle, and Austin dropped.

Certainly, a lot of R&D takes place outside universities and those figures are not included in these totals. So, these numbers are an indicator of our commitment to idea generation in academic settings, which has been an important source of innovation in Silicon Valley over the decades. Does that fact that we have lagged the national average in long-term R&D growth a cause for concern?

Clearly, decreasing federal funding for basic research is an important factor. Still, some regions have fared better than others – and this may be because universities in these regions have diversified and expanded their sources of R&D funds as the federal pie has shrunk. Universities increasingly leverage other non-federal sources of R&D funding including funds from state and local government, business, nonprofit organizations, and the institution’s own funds.

In 2014, 54 percent of total R&D expenditures in Silicon Valley’s universities came from the Federal government, the lowest of the innovation regions. At the same time, a diversified set of funding sources is likely to be a more sustainable source of R&D funds.

Silicon Valley does match Boston in overall university-based R&D expenditures, even though Boston has a larger number of institutions. But, what about the fact that Southern California and New York City both have substantially higher levels of university-based R&D investment than Silicon Valley? Does it matter and should we care? If so, what should we be doing about it? Let us know what you think.

John Melville is Co-CEO of Collaborative Economics.